Good Life Advisors – Talking Points – Week 39

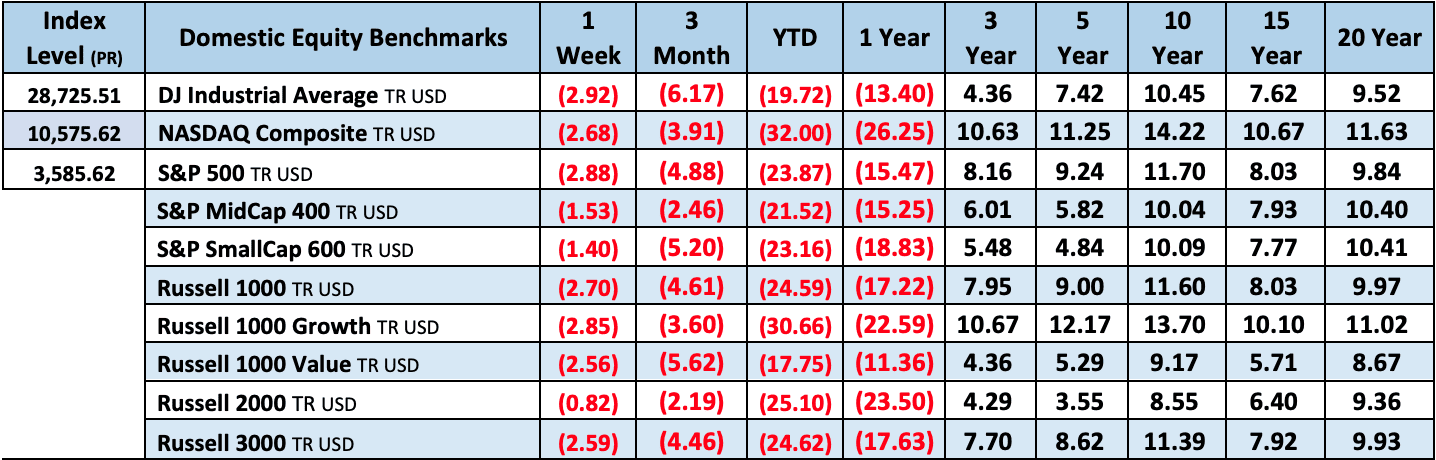

Bearish talking points pile up – Stocks down for a third straight quarter:

Treasuries came under pressure with the yield curve hitting the most inverted level this century. Two-year yields were up nearly 130 bp to just over 4.2% and ten-year yields up 85 bp to just over 3.8%. The peak Fed Funds rate at the end of the quarter was 4.45% (Apr-23), up from 3.3% (Dec-22) just after the July FOMC meeting. The dollar index jumped over 7%, it’s fifth straight quarterly gain and the largest since Q1 2015. Gold was down 7.5%. WTI crude lost nearly 25%.

The big story for Q3 was the pronounced tightening of financial conditions driven by expectations for a more aggressive global rate hike cycle. The Fed was quick to push back after the market seemed to conflate some nascent peak inflation developments with a 2023 policy pivot that at one point featured ~70 bp+ of easing. Fed officials ratcheted up the central bank’s raise-and-hold/ higher-for-longer messaging as the quarter progressed. Fed hawkishness was underpinned by hotter August core CPI data that played into concerns surrounding some of the stickier components, particularly rents. Further support came from a still tight labor market, which Fed Chair Powell noted at his September FOMC press conference had only shown modest evidence of cooling off. Labor as a lagging indicator drove a pickup in hard-landing concerns, which were also evidenced via the further inversion of the yield curve. The end of the quarter also brought a ramp in worries that tighter financial conditions (in combination with liquidity issues) were leading to meaningful stress and setting the stage for “something to break”. These fears were essentially validated by intervention episodes in both bonds and FX. In terms of the former, much of the focus was on the BoE’s announcement that it would purchase longer-dated Gilts to restore orderly market functioning following the backlash surrounding the new Truss government’s tax cut plans. On the FX front, Japan intervened to support the yen for the first time since 1998.

While the global tightening cycle dominated the bearish narrative in Q3, another big overhand on risk sentiment seemed to be concerns that earnings could be the next shoe to drop. Morgan Stanley was particularly vocal on this front, arguing that consensus estimates are too high given the combination of demand destruction, margin pressure and a stronger dollar. The firm said in mid-September that its base estimate for 2023 S&P 500 EPS is $212, ~13% below consensus, while the buy side seemed to be closer to $225, about half as bad as its forecasted cut. BofA pointed out that consensus expectations for 2023 S&P 500 EPS have only been dialed back a bit since the beginning of the year vs a typical cut of 5% at this point. It added that the Street still expects above-trend earnings growth of ~8% in 2023, while US recessions o average see 20% EPS declines. While the broader takeaway from Q2 earnings may have been that results and (particularly) guidance were better than feared, the pervasive negative sentiment in the market during much of August and September also kept some focus on elevated recession mentions and softer demand messaging. Other areas of caution included margin pressure in retail from elevated inventories stemming from both inflation and economic normalization, longer deal cycles in tech and some dialing back of hiring plans and even layoffs in harder areas like the mortgage space.

There were lots of other bearish talking points in Q3. Geopolitical tensions remained elevated even as Ukraine fared well with its counteroffensive. Russia continued to weaponize energy flows, annexed four Ukrainian regions and ratcheted up its nuclear warnings. In addition, the rhetoric between the US and China over Taiwan further heated up. Some of the interventionist developments played into worries that a (debt) financialized global economy may not be able to withstand the ferocity of the tightening cycle. They also played into worries about structural inflation pressures. There were some canary in the coalmine concerns surrounding FedEx’s earnings/ guidance blowup and the Citrix buyout loans. Negative seasonality was flagged during the September selloff, as was the dampened buyback activity ahead of quarter-end and the start of Q3 earnings season. Despite the magnitude of the selling pressure in September, there were still thoughts that the market had yet to see sufficient capitulation, particularly with the inflation fight having knocked the Fed put deeply out of the money. US equity inflows were still running at over $100B on a year-to-date basis late in the quarter. Barclays pointed out that only 0.3% of the inflows over the past two years have been reversed vs 2.6% on average in past recessions. The momentum behind the risk-off narrative put some late-quarter focus on the bear-case scenarios for stocks, with strategists flagging a 3000-3150 range for the S&P.

Trying to find some light at the end of the tunnel; One of the most positive developments in the 3rd quarter seemed to be the traction behind the peak inflation narrative. There were multiple inputs, including a 99-day stretch of declines in US gasoline prices. Median one- and three-year inflation expectations in the New York Fed survey continued their steep declines in August. Inflation components of several of the regional manufacturing surveys also softened sequentially in September. In addition, apartment rents fell for the first time in nearly two years in July, US home prices saw their biggest sequential decline on record in July, and lumber prices were off more than 70% from their March peak late in the quarter, back to pre-Covid levels. Q2 earnings season generated a lot of “better-than-feared” takeaways, there was plenty of commentary about relatively stable demand (including during the September sell-side conferences) and pricing power continued to protect margins. In addition, capital return and capex were mentioned as relative bright spots and companies flagged easing labor shortages and supply chain constraints. With so much focus on the bearish talking points, depressed sentiment and positioning indicators were flagged contrarian buy signals. The AAII bull-bear spread fell to the sixth most negative reading in the survey’s history late in the quarter, while the BofA Bull & Bear Indicator was at the max “bearish” level of 0.0 and the Goldman Sachs positioning indicator hit -1.5, signaling “extremely light” positioning.

Fixed Income

If the year ended today it would mark the worst return in bonds since 1926- The US bond aggregate is down over 14% for the year and currently in the 26 month drawdown.

Yield Curve

September FOMC Statement July Fed Minutes Balance Sheet Reduction Plan Credit, Liquidity and Balance Sheet Federal Reserve Dot Plots Treasury.gov yields FOMC Policy Normalization Statement Longer- Run Goals Jan 2022

Foreign Exchange Market

The dollar also remains a growing headwind, with the dollar index hitting the highest level since Jun-2002 this week. Dollar strength was propelled by factors including a more hawkish Fed than expected and global growth concerns. The rally also came despite a BoJ intervention to keep the yen from weakening further against the dollar (FT). Sterling weakness was the other big FX this week, falling to the lowest level against the dollar since 1985 on worries that tax cuts and energy subsidies would put the UK on an unstable fiscal path (FT). A number of analysts warned that the cycle of Fed hikes and stronger dollar may be pushing global currency toward the verge of breaking, adding to global recession fears.

As the US dollar surges, American buyers splurge on European homes – So says the WSJ

Energy Complex

The Baker Hughes rig count increased by 1 this week. There are 765 oil and gas rigs operating in the US- Up 237 over last year.

Metals Complex

Employment Picture

Weekly Unemployment Claims – Released Thursday 9/29/2022 – The week ending September 24th observed a decrease of 16k in initial claims increasing to 193k. The four-week moving average of initial jobless claims decreased 8.75k to 207k.

August Jobs Report – BLS Summary – Released 9/2/2022 – The US Economy added 315k nonfarm jobs in August and the Unemployment rate stayed increased to 3.7%. Average hourly earnings increased 10 cents to $32.36. Hiring highlights include +68k Education and Health Services, +68k Professional and Business Services, and +44k Retail Trade.

- Average hourly earnings increased 10 cents to $32.36.

- U3 unemployment rate remained increased 0.2% to 3.7%. U6 unemployment rate increased 0.3% to 7%.

- The labor force participation rate was increased 0.3% to 62.4%.

- Average work week decreased 0.1 to 34.5 hours.

Job Openings & Labor Turnover Survey – JOLTS – Released 8/30/2022 – The US Bureau of Labor Statistics reported the number and rate of job openings was little changed at 11.2 million on the last business day of July. Over the month, hires were little changed at 6.3 million and separations were little changed at 5.9 million. Within separations, quits were little changed at 4.2 million. The layoffs and discharges rates were little changed at 1.4 million.

Employment Cost Index – Released 7/29/2022 – Compensation costs for civilian workers increased 1.3% for the 3-month period ending in June 2022. The 12-month period ending in June 2022 saw compensation costs increase by 5.1%. The 12-month period ending June 2021 increased 2.1%. Wages and salaries increased 5.3% over the year and increased 3.2% for the 12-month period ending in June 2021. Benefit costs increased 4.8% over the year and increased 2.2% for the 12-month period ending in June 2021. This report is published quarterly.

This Week’s Economic Data

Links take you to the data source

Chicago PMI – Released 9/30/2022 – Chicago PMI declined sharply in September from 52.2 to 45.7.

Personal Income – Released 9/30/2022 – Personal income increased $71.6 billion or 0.3% in August according to estimates released today by the Bureau of Economic Analysis. Disposable Personal Income (DPI) increased $67.6 billion or 0.4% and Personal Consumption Expenditures (PCE) increased $67.5 billion or 0.4%.

Third Estimate of 2nd Quarter 2022 GDP – Released 9/29/2022 – Real Gross DOmestic Product (GDP) decreased at an annual rate of 0.6% in the second quarter of 2022, according to the third estimate released by the Bureau of Economic Analysis. GDP decreased 1.6% in the first quarter of 2022. Two quarters of negative GDP growth marks a technical recession. The GDP estimate released today is based on source data that are more complete than that of the second estimate which saw real GDP decline 0.6% and the advance estimate and which saw real GDP decline 0.9% in the second quarter of 2022. The decrease in real GDP reflected decreases in private inventory investment, residential fixed investment, federal government spending, state and local government spending, and nonresidential fixed investment that were partly offset by increases in exports and Personal Consumption Expenditures (PCE). Imports, which are a subtraction in the calculation of GDP, increased. The update primarily reflected an upward revision to consumer spending that was offset by a downward revision to exports. Imports, which are a subtraction in the calculation of GDP, were revised down.

Consumer Confidence – Released 9/27/2022 – The Consumer Confidence Index increased in September following an increase in August. The Index now stands at 108, up from 103.6 in August.

Durable Goods – Released 9/27/2022 – New orders for manufactured durable goods in August decreased $0.6 billion or 0.2% to $272.7 billion. Transportation equipment led the decrease down $1 billion or 1.1% to $92 billion.

New Residential Sales – Released 9/27/2022 – Sales of new single-family homes increased 28.8% to 685k, seasonally adjusted, in August. The median sales price of new homes sold in August was $436,800 with an average sales price of $521,800. At the end of August, the seasonally adjusted estimate of new homes for sale was 461k. This represents a supply of 8.1 months at the current sales rate.

Recent Economic Data

Links take you to the data source

Existing Home Sales – Released 9/21/2022 – Existing home sales decreased slightly in August marking seven consecutive months of declines. Sales declined 0.4% to a seasonally adjusted rate of 4.8 million in August. Sales decreased 19.9% year-over-year. Housing inventory sits at 1.28 million units, down 1.5% from July’s inventory, unchanged over last year. Unsold inventory sits at a 3.2-month supply. The median existing home price for all housing types was $385,500 which is up 7.7% from August 2021. This marks 126 consecutive months of year-over-year increases, the longest-running streak on record.

Housing Starts – Released 9/20/2022 – New home starts in August were at a seasonally adjusted annual rate of 1.575 million; up 12.2% above July, but 0.1% below last August’s rate. Building Permits were at a seasonally adjusted annual rate of 1.5117 million, down 10% compared to July, and down 14.4% over last year.

Retail Sales – Released 9/15/2022 – US retail sales for August increased 0.3% to $683.3 billion and retail sales are 9.1% above August 2021. US retail sales for the June 2022 through August 2022 period were up 9.3% from the same period a year ago.

Industrial Production and Capacity Utilization – Released 9/15/2022 – In August, Industrial production decreased 0.2%. Manufacturing increased 0.1%. Utilities output decreased 2.3%. Mining output was unchanged. Total industrial production was 3.7% higher in August than a year ago. Total capacity utilization decreased 0.2% in August to 80% which is 0.4% above its long run average.

Producer Price Index – Released 9/14/2022 – The Producer Price Index for final demand 0.1% in August. PPI less food and energy increased 0.2%. The change in PPI for final demand has increased 8.7% year/y.

Consumer Price Index – Released 9/13/2022 – Consumer price increased 0.1% m/m in August following no change in July. Consumer prices are up 8.3% for the 12-month period ending in August. Core consumer prices increased 0.6% m/m in August.

Consumer Credit – Released 9/8/2022 – Consumer credit increased at a seasonally adjusted annual rate of 6.2% in July 2022. Revolving credit increased at an annual rate of 11.6%, while nonrevolving credit increased at an annual rate of 4.4%.

U.S. Trade Balance – Released 9/7/2022 – According to the US Census Bureau of Economic Analysis the goods and services deficit decreased in July by $10.2 billion to $70.6 billion. July exports were $259.3 billion, $0.5 billion more than June exports. July imports were $329.9 billion, $9.7 billion less than June imports. Year to date, the goods and services deficit increased $136.6 billion, or 29%, from the same period in 2021. Exports increased $286.4 billion or 19.9%. Imports increased $423 billion or 22.1 percent.

PMI Non-Manufacturing Index – Released 9/6/2022 – Economic activity in the non-manufacturing sector grew in August for the 27th consecutive month. ISM Non-Manufacturing registered 56.9%, which is 0.2% above the July reading of 56.7%.

US Light Vehicle Sales – Released 9/2/2022 – US light vehicle sales were at a seasonally adjusted annual rate of 13.181 million units in August.

PMI Manufacturing Index – Released 9/1/2022 – Economic activity in the Non-Manufacturing sector grew in August for the 27th consecutive month. ISM Non-Manufacturing registered $136.6 billion, or 29%, from the same period in 2021. Exports increased $286.4 billion or 19.9%. Imports increased $423 billion or 22.1%.

U.S. Construction Spending – Released 9/1/2022 – Construction spending decreased 0.4% in July measuring at a seasonally adjusted annual rate of $1,777.3 billion. The July figure is 8.5% above the July 2021 estimate. Private construction spending declined 0.8% from the revised June estimate at $1,436.3 billion. Public construction spending was 1.5% above the revised June estimate at $353.1 billion.

Next week we get data on US Construction Spending, Manufacturing PMI, the US Trade Balance, Consumer Credit, JOLTS, and the September Jobs Report.

Data Sources:

Bureau of Economic Analysis (BEA)

Congressional Budget Office (CBO)

U.S. Bureau of Labor Statistics (BLS)

Federal Reserve Economic Data (FRED Charts)

CME Fed Watch

U.S. Treasury – Yields

U.S. Census Bureau

Institute for Supply Management (ISM)

Weekly DOL Employment Data

BLS Monthly Jobs Report

JOLTS

US Energy Admin (EIA)

BLS Consumer Price Index CPI

BLS Producer Price Index PPI

Atlanta Fed GDPNOW

NY Fed Nowcast GDP

US Census Bureau Housing Starts

Consumer Credit

USCB Retail Sales

Construction Spending

Federal Reserve Dot Plots

NY Empire Index

Philadelphia Federal Reserve

P/E Ratio Data -Yardeni Research

Technical Analysis Info:

StockCharts.com – Financial Charts

Exponential vs Simple moving average

Other Links:

1973 Arab Oil Embargo

Hunt Brothers Silver

Long-Term Capital bailout

Table of Contents

Good Life Advisors – Talking Points – Week 39

Bearish talking points pile up – Stocks down for a third straight quarter:

Treasuries came under pressure with the yield curve hitting the most inverted level this century. Two-year yields were up nearly 130 bp to just over 4.2% and ten-year yields up 85 bp to just over 3.8%. The peak Fed Funds rate at the end of the quarter was 4.45% (Apr-23), up from 3.3% (Dec-22) just after the July FOMC meeting. The dollar index jumped over 7%, it’s fifth straight quarterly gain and the largest since Q1 2015. Gold was down 7.5%. WTI crude lost nearly 25%.

The big story for Q3 was the pronounced tightening of financial conditions driven by expectations for a more aggressive global rate hike cycle. The Fed was quick to push back after the market seemed to conflate some nascent peak inflation developments with a 2023 policy pivot that at one point featured ~70 bp+ of easing. Fed officials ratcheted up the central bank’s raise-and-hold/ higher-for-longer messaging as the quarter progressed. Fed hawkishness was underpinned by hotter August core CPI data that played into concerns surrounding some of the stickier components, particularly rents. Further support came from a still tight labor market, which Fed Chair Powell noted at his September FOMC press conference had only shown modest evidence of cooling off. Labor as a lagging indicator drove a pickup in hard-landing concerns, which were also evidenced via the further inversion of the yield curve. The end of the quarter also brought a ramp in worries that tighter financial conditions (in combination with liquidity issues) were leading to meaningful stress and setting the stage for “something to break”. These fears were essentially validated by intervention episodes in both bonds and FX. In terms of the former, much of the focus was on the BoE’s announcement that it would purchase longer-dated Gilts to restore orderly market functioning following the backlash surrounding the new Truss government’s tax cut plans. On the FX front, Japan intervened to support the yen for the first time since 1998.

While the global tightening cycle dominated the bearish narrative in Q3, another big overhand on risk sentiment seemed to be concerns that earnings could be the next shoe to drop. Morgan Stanley was particularly vocal on this front, arguing that consensus estimates are too high given the combination of demand destruction, margin pressure and a stronger dollar. The firm said in mid-September that its base estimate for 2023 S&P 500 EPS is $212, ~13% below consensus, while the buy side seemed to be closer to $225, about half as bad as its forecasted cut. BofA pointed out that consensus expectations for 2023 S&P 500 EPS have only been dialed back a bit since the beginning of the year vs a typical cut of 5% at this point. It added that the Street still expects above-trend earnings growth of ~8% in 2023, while US recessions o average see 20% EPS declines. While the broader takeaway from Q2 earnings may have been that results and (particularly) guidance were better than feared, the pervasive negative sentiment in the market during much of August and September also kept some focus on elevated recession mentions and softer demand messaging. Other areas of caution included margin pressure in retail from elevated inventories stemming from both inflation and economic normalization, longer deal cycles in tech and some dialing back of hiring plans and even layoffs in harder areas like the mortgage space.

There were lots of other bearish talking points in Q3. Geopolitical tensions remained elevated even as Ukraine fared well with its counteroffensive. Russia continued to weaponize energy flows, annexed four Ukrainian regions and ratcheted up its nuclear warnings. In addition, the rhetoric between the US and China over Taiwan further heated up. Some of the interventionist developments played into worries that a (debt) financialized global economy may not be able to withstand the ferocity of the tightening cycle. They also played into worries about structural inflation pressures. There were some canary in the coalmine concerns surrounding FedEx’s earnings/ guidance blowup and the Citrix buyout loans. Negative seasonality was flagged during the September selloff, as was the dampened buyback activity ahead of quarter-end and the start of Q3 earnings season. Despite the magnitude of the selling pressure in September, there were still thoughts that the market had yet to see sufficient capitulation, particularly with the inflation fight having knocked the Fed put deeply out of the money. US equity inflows were still running at over $100B on a year-to-date basis late in the quarter. Barclays pointed out that only 0.3% of the inflows over the past two years have been reversed vs 2.6% on average in past recessions. The momentum behind the risk-off narrative put some late-quarter focus on the bear-case scenarios for stocks, with strategists flagging a 3000-3150 range for the S&P.

Trying to find some light at the end of the tunnel; One of the most positive developments in the 3rd quarter seemed to be the traction behind the peak inflation narrative. There were multiple inputs, including a 99-day stretch of declines in US gasoline prices. Median one- and three-year inflation expectations in the New York Fed survey continued their steep declines in August. Inflation components of several of the regional manufacturing surveys also softened sequentially in September. In addition, apartment rents fell for the first time in nearly two years in July, US home prices saw their biggest sequential decline on record in July, and lumber prices were off more than 70% from their March peak late in the quarter, back to pre-Covid levels. Q2 earnings season generated a lot of “better-than-feared” takeaways, there was plenty of commentary about relatively stable demand (including during the September sell-side conferences) and pricing power continued to protect margins. In addition, capital return and capex were mentioned as relative bright spots and companies flagged easing labor shortages and supply chain constraints. With so much focus on the bearish talking points, depressed sentiment and positioning indicators were flagged contrarian buy signals. The AAII bull-bear spread fell to the sixth most negative reading in the survey’s history late in the quarter, while the BofA Bull & Bear Indicator was at the max “bearish” level of 0.0 and the Goldman Sachs positioning indicator hit -1.5, signaling “extremely light” positioning.

Fixed Income

If the year ended today it would mark the worst return in bonds since 1926- The US bond aggregate is down over 14% for the year and currently in the 26 month drawdown.

Yield Curve

September FOMC Statement July Fed Minutes Balance Sheet Reduction Plan Credit, Liquidity and Balance Sheet Federal Reserve Dot Plots Treasury.gov yields FOMC Policy Normalization Statement Longer- Run Goals Jan 2022

Foreign Exchange Market

The dollar also remains a growing headwind, with the dollar index hitting the highest level since Jun-2002 this week. Dollar strength was propelled by factors including a more hawkish Fed than expected and global growth concerns. The rally also came despite a BoJ intervention to keep the yen from weakening further against the dollar (FT). Sterling weakness was the other big FX this week, falling to the lowest level against the dollar since 1985 on worries that tax cuts and energy subsidies would put the UK on an unstable fiscal path (FT). A number of analysts warned that the cycle of Fed hikes and stronger dollar may be pushing global currency toward the verge of breaking, adding to global recession fears.

As the US dollar surges, American buyers splurge on European homes – So says the WSJ

Energy Complex

The Baker Hughes rig count increased by 1 this week. There are 765 oil and gas rigs operating in the US- Up 237 over last year.

Metals Complex

Employment Picture

Weekly Unemployment Claims – Released Thursday 9/29/2022 – The week ending September 24th observed a decrease of 16k in initial claims increasing to 193k. The four-week moving average of initial jobless claims decreased 8.75k to 207k.

August Jobs Report – BLS Summary – Released 9/2/2022 – The US Economy added 315k nonfarm jobs in August and the Unemployment rate stayed increased to 3.7%. Average hourly earnings increased 10 cents to $32.36. Hiring highlights include +68k Education and Health Services, +68k Professional and Business Services, and +44k Retail Trade.

Job Openings & Labor Turnover Survey – JOLTS – Released 8/30/2022 – The US Bureau of Labor Statistics reported the number and rate of job openings was little changed at 11.2 million on the last business day of July. Over the month, hires were little changed at 6.3 million and separations were little changed at 5.9 million. Within separations, quits were little changed at 4.2 million. The layoffs and discharges rates were little changed at 1.4 million.

Employment Cost Index – Released 7/29/2022 – Compensation costs for civilian workers increased 1.3% for the 3-month period ending in June 2022. The 12-month period ending in June 2022 saw compensation costs increase by 5.1%. The 12-month period ending June 2021 increased 2.1%. Wages and salaries increased 5.3% over the year and increased 3.2% for the 12-month period ending in June 2021. Benefit costs increased 4.8% over the year and increased 2.2% for the 12-month period ending in June 2021. This report is published quarterly.

This Week’s Economic Data

Links take you to the data source

Chicago PMI – Released 9/30/2022 – Chicago PMI declined sharply in September from 52.2 to 45.7.

Personal Income – Released 9/30/2022 – Personal income increased $71.6 billion or 0.3% in August according to estimates released today by the Bureau of Economic Analysis. Disposable Personal Income (DPI) increased $67.6 billion or 0.4% and Personal Consumption Expenditures (PCE) increased $67.5 billion or 0.4%.

Third Estimate of 2nd Quarter 2022 GDP – Released 9/29/2022 – Real Gross DOmestic Product (GDP) decreased at an annual rate of 0.6% in the second quarter of 2022, according to the third estimate released by the Bureau of Economic Analysis. GDP decreased 1.6% in the first quarter of 2022. Two quarters of negative GDP growth marks a technical recession. The GDP estimate released today is based on source data that are more complete than that of the second estimate which saw real GDP decline 0.6% and the advance estimate and which saw real GDP decline 0.9% in the second quarter of 2022. The decrease in real GDP reflected decreases in private inventory investment, residential fixed investment, federal government spending, state and local government spending, and nonresidential fixed investment that were partly offset by increases in exports and Personal Consumption Expenditures (PCE). Imports, which are a subtraction in the calculation of GDP, increased. The update primarily reflected an upward revision to consumer spending that was offset by a downward revision to exports. Imports, which are a subtraction in the calculation of GDP, were revised down.

Consumer Confidence – Released 9/27/2022 – The Consumer Confidence Index increased in September following an increase in August. The Index now stands at 108, up from 103.6 in August.

Durable Goods – Released 9/27/2022 – New orders for manufactured durable goods in August decreased $0.6 billion or 0.2% to $272.7 billion. Transportation equipment led the decrease down $1 billion or 1.1% to $92 billion.

New Residential Sales – Released 9/27/2022 – Sales of new single-family homes increased 28.8% to 685k, seasonally adjusted, in August. The median sales price of new homes sold in August was $436,800 with an average sales price of $521,800. At the end of August, the seasonally adjusted estimate of new homes for sale was 461k. This represents a supply of 8.1 months at the current sales rate.

Recent Economic Data

Links take you to the data source

Existing Home Sales – Released 9/21/2022 – Existing home sales decreased slightly in August marking seven consecutive months of declines. Sales declined 0.4% to a seasonally adjusted rate of 4.8 million in August. Sales decreased 19.9% year-over-year. Housing inventory sits at 1.28 million units, down 1.5% from July’s inventory, unchanged over last year. Unsold inventory sits at a 3.2-month supply. The median existing home price for all housing types was $385,500 which is up 7.7% from August 2021. This marks 126 consecutive months of year-over-year increases, the longest-running streak on record.

Housing Starts – Released 9/20/2022 – New home starts in August were at a seasonally adjusted annual rate of 1.575 million; up 12.2% above July, but 0.1% below last August’s rate. Building Permits were at a seasonally adjusted annual rate of 1.5117 million, down 10% compared to July, and down 14.4% over last year.

Retail Sales – Released 9/15/2022 – US retail sales for August increased 0.3% to $683.3 billion and retail sales are 9.1% above August 2021. US retail sales for the June 2022 through August 2022 period were up 9.3% from the same period a year ago.

Industrial Production and Capacity Utilization – Released 9/15/2022 – In August, Industrial production decreased 0.2%. Manufacturing increased 0.1%. Utilities output decreased 2.3%. Mining output was unchanged. Total industrial production was 3.7% higher in August than a year ago. Total capacity utilization decreased 0.2% in August to 80% which is 0.4% above its long run average.

Producer Price Index – Released 9/14/2022 – The Producer Price Index for final demand 0.1% in August. PPI less food and energy increased 0.2%. The change in PPI for final demand has increased 8.7% year/y.

Consumer Price Index – Released 9/13/2022 – Consumer price increased 0.1% m/m in August following no change in July. Consumer prices are up 8.3% for the 12-month period ending in August. Core consumer prices increased 0.6% m/m in August.

Consumer Credit – Released 9/8/2022 – Consumer credit increased at a seasonally adjusted annual rate of 6.2% in July 2022. Revolving credit increased at an annual rate of 11.6%, while nonrevolving credit increased at an annual rate of 4.4%.

U.S. Trade Balance – Released 9/7/2022 – According to the US Census Bureau of Economic Analysis the goods and services deficit decreased in July by $10.2 billion to $70.6 billion. July exports were $259.3 billion, $0.5 billion more than June exports. July imports were $329.9 billion, $9.7 billion less than June imports. Year to date, the goods and services deficit increased $136.6 billion, or 29%, from the same period in 2021. Exports increased $286.4 billion or 19.9%. Imports increased $423 billion or 22.1 percent.

PMI Non-Manufacturing Index – Released 9/6/2022 – Economic activity in the non-manufacturing sector grew in August for the 27th consecutive month. ISM Non-Manufacturing registered 56.9%, which is 0.2% above the July reading of 56.7%.

US Light Vehicle Sales – Released 9/2/2022 – US light vehicle sales were at a seasonally adjusted annual rate of 13.181 million units in August.

PMI Manufacturing Index – Released 9/1/2022 – Economic activity in the Non-Manufacturing sector grew in August for the 27th consecutive month. ISM Non-Manufacturing registered $136.6 billion, or 29%, from the same period in 2021. Exports increased $286.4 billion or 19.9%. Imports increased $423 billion or 22.1%.

U.S. Construction Spending – Released 9/1/2022 – Construction spending decreased 0.4% in July measuring at a seasonally adjusted annual rate of $1,777.3 billion. The July figure is 8.5% above the July 2021 estimate. Private construction spending declined 0.8% from the revised June estimate at $1,436.3 billion. Public construction spending was 1.5% above the revised June estimate at $353.1 billion.

Next week we get data on US Construction Spending, Manufacturing PMI, the US Trade Balance, Consumer Credit, JOLTS, and the September Jobs Report.

Data Sources:

Bureau of Economic Analysis (BEA)

Congressional Budget Office (CBO)

U.S. Bureau of Labor Statistics (BLS)

Federal Reserve Economic Data (FRED Charts)

CME Fed Watch

U.S. Treasury – Yields

U.S. Census Bureau

Institute for Supply Management (ISM)

Weekly DOL Employment Data

BLS Monthly Jobs Report

JOLTS

US Energy Admin (EIA)

BLS Consumer Price Index CPI

BLS Producer Price Index PPI

Atlanta Fed GDPNOW

NY Fed Nowcast GDP

US Census Bureau Housing Starts

Consumer Credit

USCB Retail Sales

Construction Spending

Federal Reserve Dot Plots

NY Empire Index

Philadelphia Federal Reserve

P/E Ratio Data -Yardeni Research

Technical Analysis Info:

StockCharts.com – Financial Charts

Exponential vs Simple moving average

Other Links:

1973 Arab Oil Embargo

Hunt Brothers Silver

Long-Term Capital bailout

Categories:

Tags: